Are you familiar with MACRS Depreciation? If not, you’re not alone. Many individuals and businesses struggle to understand the complexities of depreciation and how it impacts their financials. In this blog post, we will delve into the world of MACRS Depreciation, providing you with clear explanations, calculations, and real-life examples to demystify this important concept

Depreciation can be a confusing and overwhelming topic, often leaving individuals scratching their heads. It’s common to feel perplexed when trying to navigate through the intricate calculations and rules surrounding MACRS Depreciation. However, acknowledging this challenge is the first step towards gaining a solid grasp of the subject.

Fear not! Our aim is to simplify the complexities of MACRS Depreciation and equip you with the knowledge and tools to confidently handle depreciation in your financial endeavors. We understand that unraveling the intricacies of depreciation can seem daunting, but we assure you that by the end of this blog post, you’ll have a clear understanding of MACRS Depreciation and its calculations.

Also Read: Rulesofcheaters: Game Hacks and Cheats for Free

What is MACRS Depreciation?

MACRS Depreciation plays a vital role in financial planning, particularly when it comes to managing assets and tax implications. To understand its significance, let’s delve into the concept of MACRS Depreciation and how it affects businesses.

Explanation of MACRS Depreciation

MACRS, which stands for Modified Accelerated Cost Recovery System, is a depreciation method used by businesses to recover the cost of tangible assets over their useful lives. It allows businesses to deduct the cost of these assets from their taxable income, thereby reducing their tax liability. MACRS Depreciation provides a systematic way of allocating the cost of an asset over time, reflecting its gradual decline in value due to wear and tear, obsolescence, or other factors.

Importance and relevance of MACRS Depreciation in financial planning

Effective financial planning is crucial for businesses to optimize their cash flow and make informed decisions about investing in new assets. MACRS Depreciation offers several advantages in this regard. By allowing businesses to deduct the cost of assets over time, it helps in accurately representing the decline in value and the actual expense incurred. This, in turn, enables better tracking of profits, helps with budgeting, and facilitates long-term financial forecasting.

Moreover, MACRS Depreciation provides businesses with tax benefits. By deducting a portion of the asset’s cost each year, businesses can lower their taxable income, resulting in reduced tax liability. This frees up funds that can be reinvested in the business or used for other purposes, fostering growth and financial stability.

How Does MACRS Depreciation Work?

Now that we understand the significance of MACRS Depreciation, let’s explore how it works and the calculation process involved.

Overview of MACRS Depreciation method

MACRS Depreciation employs a specific set of rules and tables to determine the depreciation expense for each asset. It categorizes assets into different classes based on their expected useful lives, with each class having its own depreciation rates and recovery periods. The IRS (Internal Revenue Service) provides guidelines outlining these classes and the applicable depreciation methods.

Explanation of the depreciation calculation process

The depreciation calculation under MACRS involves three key factors: the asset’s cost, its recovery period, and the applicable depreciation method. The asset’s cost generally includes the purchase price along with any related expenses like transportation or installation. The recovery period depends on the asset’s classification, which can range from three to 50 years, depending on its nature and purpose. Lastly, the depreciation method determines how the asset’s cost is allocated over its recovery period.

Illustration of the depreciation formula with examples

Let’s consider an example to illustrate how MACRS Depreciation is calculated. Suppose a business purchases machinery for $50,000, and it falls under the five-year recovery period class. The applicable MACRS depreciation method for this class is the 200% declining balance method.

Using this information, we can calculate the depreciation expense for each year using the MACRS Depreciation tables and formulas provided by the IRS. For instance, in the first year, the depreciation expense would be $20,000 (40% of the asset’s cost), followed by $12,000 (24% of the remaining balance) in the second year, and so on until the asset’s cost is fully depreciated or the recovery period ends.

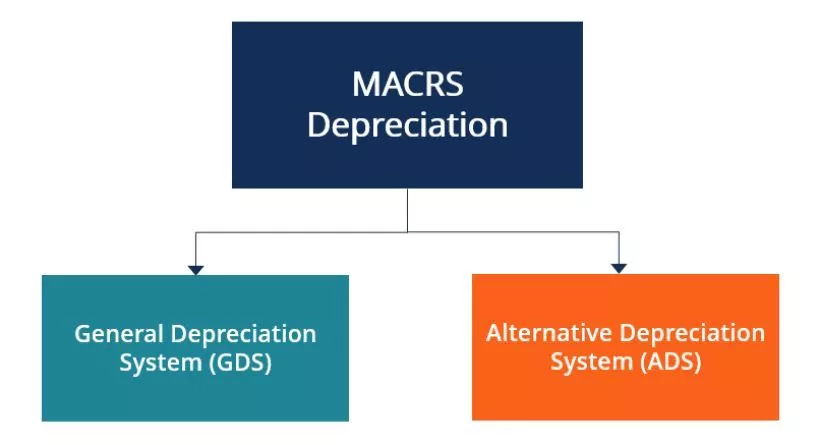

Different MACRS Depreciation Methods

When it comes to MACRS Depreciation, there are several methods available for businesses to choose from. Each method follows a specific approach to allocating the cost of assets over their recovery periods. Let’s explore the different MACRS Depreciation methods and understand their implications.

Description of different MACRS Depreciation methods

The General Depreciation System (GDS): This is the most commonly used MACRS Depreciation method. It assigns assets to specific recovery periods ranging from three to 50 years, depending on their classification. GDS uses a declining balance method, where higher depreciation expenses are incurred in the early years, gradually decreasing over time.

The Alternative Depreciation System (ADS): ADS is an alternative to GDS and is primarily used for certain types of property, such as tax-exempt entities or those involved in farming or real estate businesses. Unlike GDS, ADS employs straight-line depreciation, where the same amount is deducted each year over the asset’s recovery period.

Comparison of the methods and their implications

The choice between GDS and ADS depends on various factors, including the nature of the asset, its useful life, and the business’s specific requirements. GDS, with its accelerated depreciation, can provide larger deductions in the early years, resulting in higher tax savings. On the other hand, ADS offers a more consistent depreciation expense throughout the asset’s recovery period, providing stability and predictability in financial planning.

It’s important to note that once a MACRS Depreciation method is selected for an asset, it generally remains consistent throughout its recovery period. However, there are instances where businesses can switch from GDS to ADS or vice versa, subject to certain conditions and IRS guidelines.

Considering the implications of each method and aligning it with your business’s financial goals and tax strategy is crucial. Seeking professional advice or consulting with a tax specialist can help you make an informed decision that best suits your unique circumstances.

Also Read: Disney Plus: How to Stream Disney’s Huge Movie and TV Library

Benefits and Limitations of MACRS Depreciation

MACRS Depreciation offers several benefits to businesses, but it’s important to understand its limitations and considerations. Let’s delve into the advantages of using MACRS Depreciation and the key factors to keep in mind.

Discussion of the advantages of using MACRS Depreciation

Increased Tax Savings: MACRS Depreciation allows businesses to deduct the cost of assets over time, resulting in reduced taxable income and lower tax liability. This provides immediate cash flow benefits, enabling businesses to allocate funds towards growth initiatives or other essential expenses.

Accurate Asset Valuation: By reflecting the decline in value of assets over their useful lives, MACRS Depreciation provides a more accurate representation of the asset’s worth on the balance sheet. This aids in making informed financial decisions, such as determining the optimal time for asset replacement or resale.

Identification of the limitations and considerations to keep in mind

Recapture of Depreciation: If a business disposes of a MACRS Depreciation asset before the end of its recovery period, there may be a requirement to recapture a portion of the previously claimed depreciation. This recaptured amount is subject to ordinary income tax rates and can impact the overall tax liability.

Differences in State Tax Laws: While MACRS Depreciation is a federal tax provision, it’s important to consider state tax laws as well. Some states may have variations in depreciation rules, recovery periods, or depreciation methods. Understanding these differences and aligning them with your state’s regulations is crucial to ensure compliance and optimize tax savings.

Real-Life Examples and Financial Impact

Depreciation is an essential concept in accounting and finance that allows businesses to allocate the cost of assets over their useful lives. One widely used depreciation method is the Modified Accelerated Cost Recovery System (MACRS). In this blog post, we will explore the application of MACRS depreciation in various real-life scenarios and analyze its impact on financial statements. By understanding MACRS depreciation and its practical implications, you can make informed decisions regarding asset investments and financial planning.

Application of MACRS Depreciation in Real-Life Scenarios

Suppose you run a small consulting firm and purchase new office equipment, such as computers, printers, and furniture, with a total cost of $50,000. By applying MACRS depreciation, you can allocate the cost of these assets over their designated recovery periods. For office equipment, the recovery period is five years. Let’s assume a straight-line method with equal deductions each year. Therefore, you can claim a depreciation deduction of $10,000 per year for five years.

Imagine you’re a real estate investor and acquire a commercial property for $2 million. However, not all components of the property are subject to the same recovery period. The building itself has a recovery period of 39 years, while items like carpets and landscaping have shorter recovery periods. By leveraging MACRS depreciation, you can optimize tax savings by appropriately classifying assets and applying the corresponding recovery periods.

Analysis of Outcomes and Impact on Financial Statements

One significant advantage of MACRS depreciation is the potential for tax savings. By deducting depreciation expenses from taxable income, businesses can reduce their tax liability and improve cash flow. The timing of deductions under MACRS is accelerated, enabling businesses to benefit from larger deductions in the early years of an asset’s life.

MACRS depreciation affects financial statements by reducing the value of assets over time. As assets depreciate, their carrying value on the balance sheet decreases, impacting metrics like net book value and total assets. Additionally, the depreciation expense appears on the income statement, reducing reported profits and improving the accuracy of financial performance measurement.

Also Read: 3 Ways to Get a Free Google Ads Promo Code or Coupon in 2023

Conclusion:

In conclusion, effectively managing MACRS Depreciation is essential for optimizing tax benefits and enhancing financial planning. By understanding the concept of MACRS Depreciation, selecting the appropriate methods, staying updated with regulations, and conducting regular asset reviews, you can make the most of this depreciation system. It allows you to recover the costs of your business assets over time while maximizing your deductions.

Remember, MACRS Depreciation is a powerful tool that can significantly impact your financial statements and tax planning strategies. By implementing the tips and best practices discussed in this article, you can navigate through the complexities of MACRS Depreciation with confidence and precision.

Start by selecting the right asset classes, understanding the depreciation methods, and maintaining accurate documentation. Stay updated with the latest tax laws and regulations, and consider leveraging bonus depreciation and Section 179 provisions for additional benefits. Regularly review your assets to ensure their proper classification and make adjustments as needed.

By implementing effective MACRS Depreciation management strategies, you can optimize your financial planning and ensure compliance with tax regulations. Remember, seeking professional advice when needed is always a wise decision.

FAQs:

Q: How can I determine the MACRS class of an asset?

A: The MACRS class of an asset is determined based on its useful life. The Internal Revenue Service (IRS) provides guidelines and tables for different types of assets and their respective classes. These guidelines help determine the appropriate recovery period for depreciation calculations.

Q: Can I switch between different MACRS Depreciation methods?

A: Generally, once you choose a MACRS Depreciation method for an asset, it must be consistently applied throughout the asset’s recovery period. However, certain circumstances may allow a change in method, such as a change in business use or if you have permission from the IRS. Consult with a tax professional for guidance on changing methods.

Q: Is MACRS Depreciation applicable to all types of assets?

A: MACRS Depreciation is applicable to most tangible property used in business or income-producing activities, including machinery, equipment, buildings, and vehicles. However, certain assets may be subject to specific rules or have separate depreciation methods. Consult with a tax advisor to determine the eligibility of your assets for MACRS Depreciation.

Q: Can I claim MACRS Depreciation for assets used for personal purposes?

A: No, MACRS Depreciation is specifically for assets used in business or income-producing activities. Personal assets, such as those used for personal residence or personal vehicles, are not eligible for MACRS Depreciation. Separate rules and regulations apply to personal assets.

Q: What happens if I dispose of an asset before the end of its recovery period?

A: If you dispose of an asset before the end of its recovery period, you may need to make adjustments to the depreciation calculations. The IRS provides guidelines for determining the gain or loss on the disposition of MACRS property. Consult with a tax professional to understand the implications and reporting requirements for asset disposal.